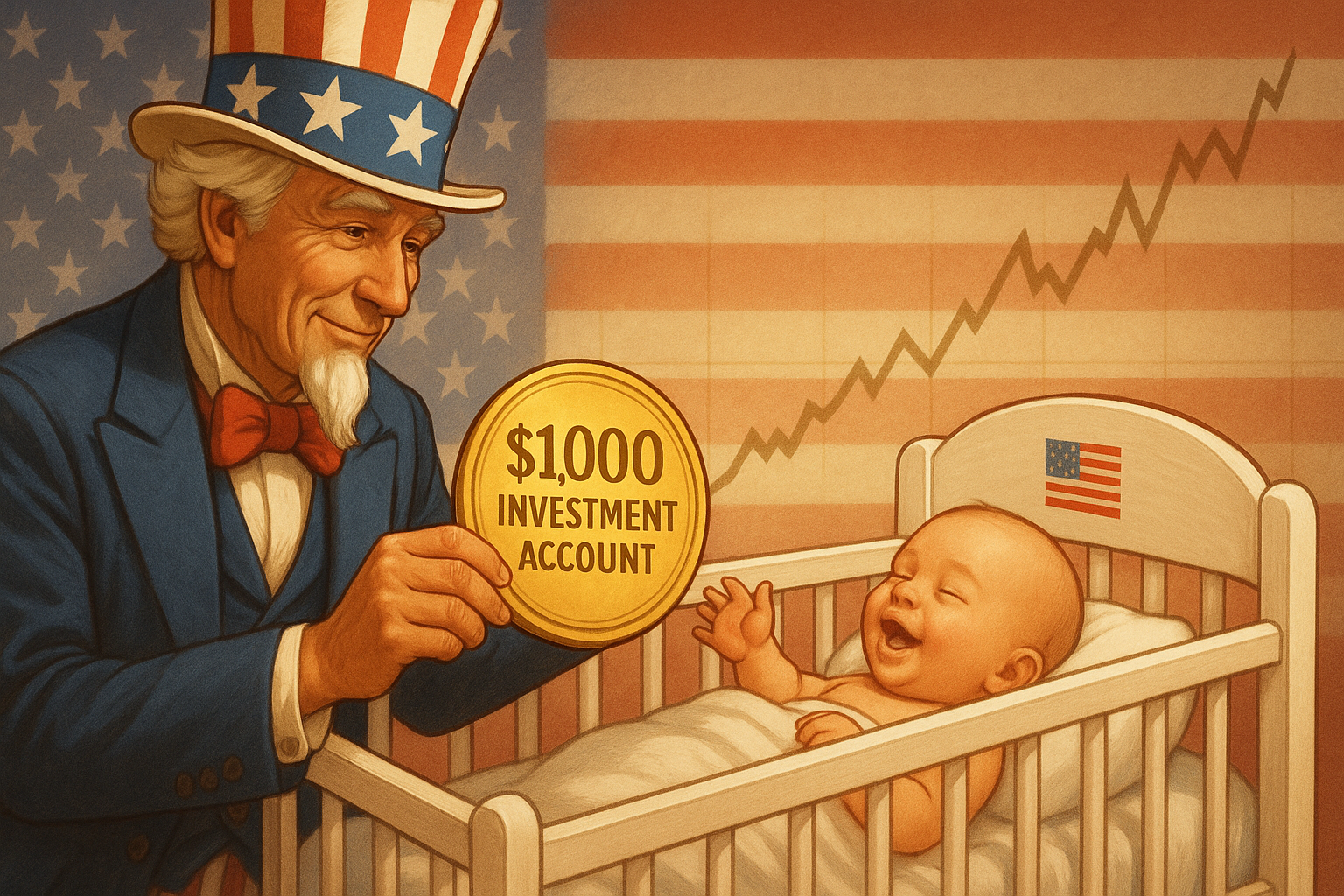

In a move that feels like it was pulled straight from a political screenwriter's fever dream, Congress actually managed to work together long enough to pass the Invest America Act—on July 4th, no less. You can't make this stuff up.

The legislation creates what might be the most ambitious financial experiment in modern American history: a $1,000 investment account for every newborn American child. It's essentially turning Uncle Sam into the nation's most prolific venture capitalist, but instead of backing the next Silicon Valley unicorn, he's backing... well, actual babies.

I've covered economic policy for years, and this one's a doozy. It's democratic capitalism with training wheels—or maybe a pacifier.

Here's the deal: Each American baby gets a grand in an investment account at birth. Family members can pile on up to $5,000 more annually. The funds grow tax-deferred until adulthood, primarily parked in boring-but-reliable S&P 500 index funds. When the kid hits 18, they can access the money, paying capital gains taxes on withdrawals.

What we're witnessing is pretty revolutionary. America is basically creating the world's largest distributed sovereign wealth fund. It's like Norway's approach, except instead of one massive piggy bank, we're giving millions of tiny ones to families across the country.

The Magic of Compound Interest (Or: How to Turn Baby Money into Adult Money)

Think about the math for a second. That initial grand, if the markets behave historically (a big if, I know), could mushroom into roughly $20,000 by high school graduation. Toss in those grandparent contributions—because what else are grandparents for?—and suddenly college doesn't seem quite so financially terrifying.

But here's what fascinates me most: the psychological shift. Imagine growing up checking stock tickers alongside TikTok. Financial literacy in this country is... well, let's be kind and call it "underdeveloped." Something like 57% of American adults can't pass basic financial literacy tests. (How the other 43% managed to pass is a question I sometimes ponder while balancing my own checkbook.)

This program creates a natural incentive for kids to understand markets, compounding, and investment fundamentals from an early age. That's huge.

Market Implications (For Those Who Care About Such Things)

Look, I'm no market analyst, but even I can do this basic math. About 3.7 million babies are born annually in the U.S. That's $3.7 billion in mandatory market inflows each year just from the seed investments. Factor in additional contributions, and we could be looking at $10-15 billion entering markets annually through these kiddie accounts.

Is that a lot? In a $50+ trillion stock market, it's practically a rounding error. But—and this is important—it's predictable, persistent capital that's structurally committed to long-term market participation. That creates a different kind of stability.

The appointment of SoFi CEO Anthony Noto to the program's oversight council is telling. He's the only financial industry exec in the mix, and SoFi knows something crucial about financial behavior: early habits stick.

Not Everyone's Popping Champagne

Of course, there are critics. Aren't there always?

Fiscal conservatives are wringing their hands about government overreach. Market skeptics worry we're essentially indoctrinating children into a capitalist system before they can even say "diversification." Some behavioral economists (a fun bunch at parties, let me tell you) raise questions about whether forced participation actually creates genuine financial literacy.

And then there's the moral hazard question. Are we creating an entire generation with a vested interest in preserving market structures that might need fundamental reform? It's worth pondering.

During a conference call with several economists last week, I heard concerns ranging from the practical to the philosophical. "We're essentially creating millions of tiny stakeholders in the status quo," said one professor who preferred not to be named because, well, academics are cautious that way.

This Is Just the Beginning

If there's one thing I've learned covering politics (besides never eating the press room sandwiches after hour three), it's that popular programs expand. The political incentives are just too perfect.

Imagine running for office on the platform: "I'll double your child's seed investment!" It costs relatively little per voter, benefits materialize well into the future, and it somehow manages to align with both conservative ideals of ownership and progressive goals of opportunity.

What we're really seeing is a subtle but profound shift in the relationship between Americans and capital markets. Stock ownership has always been optional and unevenly distributed. Now it's becoming something closer to a birthright.

The legendary investor Benjamin Graham once noted that markets are voting machines in the short run and weighing machines in the long run. With Invest America, we're creating a new class of permanent voters—kids who've never known a world where they weren't market participants.

The implications will unfold over decades, not quarters. In the meantime, I'm wondering which lucky infant will be the first Invest America millionaire. My money's on whichever baby has Warren Buffett as a godfather.

Then again, in this economy? Maybe we should all be asking for adoption papers from the Oracle of Omaha.

scene of a typical suburban mailbox standing by a quiet street. The mailbox door is open and empty, its red flag raised. An envelope stamped “$2000 Stimulus Check” drifts away o")