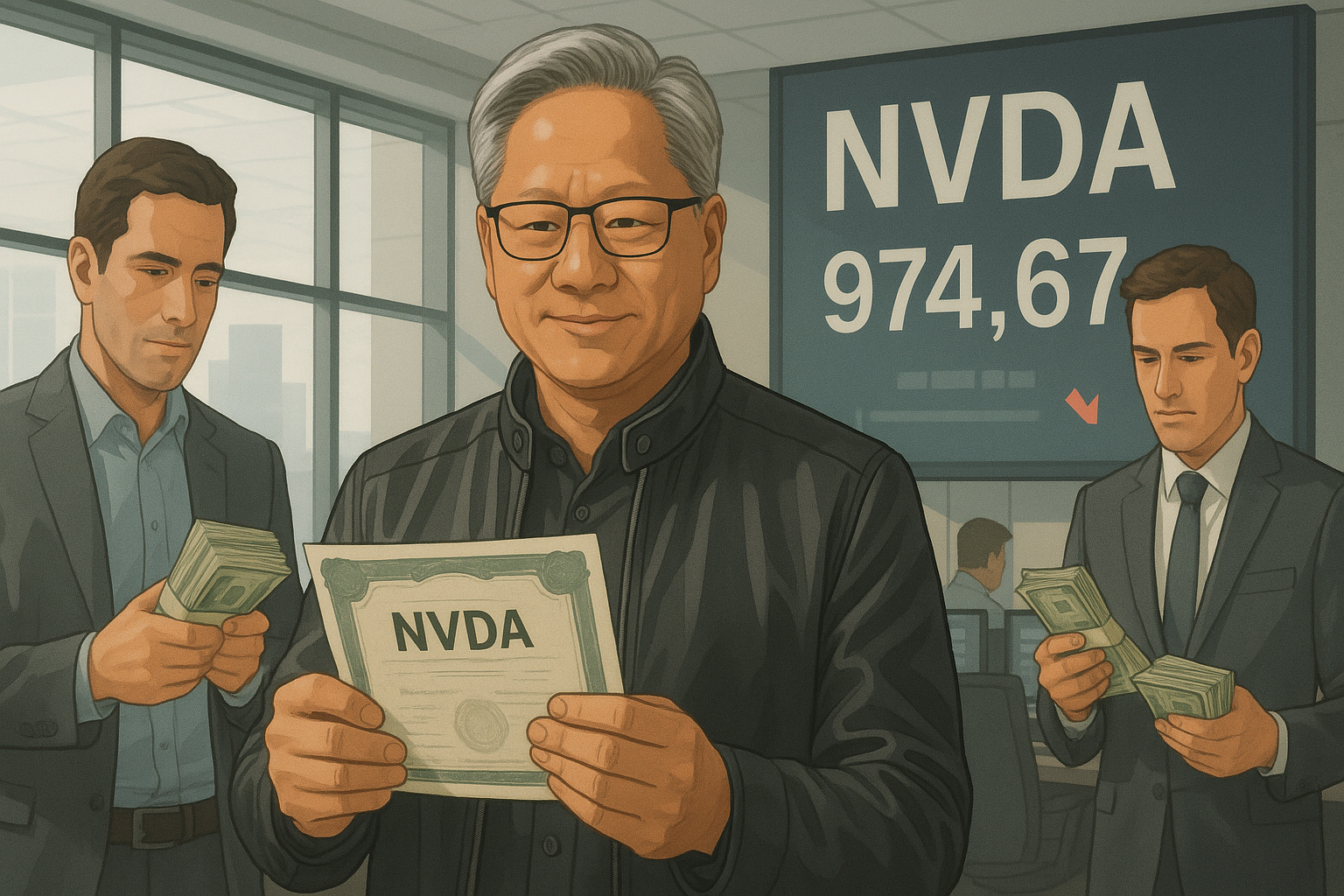

The leather jacket-wearing titan of AI and his executive team are cashing in big—really big—as Nvidia's stock price continues its stratospheric rise. And it's got Wall Street whispering.

Insiders at the chip giant have unloaded north of $1 billion in company stock over the past year, with half that amount—yes, $500 million—hitting the market just this month as shares touched all-time highs. Even Jensen Huang, the charismatic CEO who's become something of a tech folk hero, joined the selling party this week for the first time since last September.

All this while Nvidia's stock has rocketed more than 60% from April lows, riding the AI hype train and whispers of potential Trump tariff relief.

So what gives? Is this the financial equivalent of restaurant staff quietly slipping out the back door right before you order the seafood special?

I've spent the better part of a decade covering tech stocks, and let me tell you—it's complicated.

The Billion-Dollar Question

Look, insider selling at high-flying tech companies is about as surprising as finding out a streaming service raised its prices again. Executives get mountains of stock as compensation, and eventually, they want to buy things. Like houses. Or islands.

But a billion dollars? That gets attention.

What's particularly interesting (or concerning, depending on your investment stance) is the timing. This massive sell-off coincides with Nvidia hitting record valuations. You don't need an MBA to wonder if the folks with the most intimate knowledge of the company might be thinking, "Hmm, this might be getting a bit frothy."

Then again, there's an old Wall Street adage worth remembering: insiders sell for many reasons—diversification, tax planning, funding their kid's college, buying that ridiculous yacht they've always wanted. They only buy for one reason: they think the stock is going up.

Vertigo-Inducing Valuations

Have you seen Nvidia's forward P/E ratio lately? It's in nosebleed territory. (And I say that as someone who's tracked semiconductor stocks through multiple cycles.)

The bull case is compelling and well-known: Nvidia sits at the white-hot center of the AI revolution. Their GPUs are to artificial intelligence what Intel's processors were to the PC era—the essential ingredient that makes the magic happen. As one fund manager told me last week, "They're selling pickaxes in a gold rush, and everybody needs pickaxes."

But—and this is a substantial but—even revolutionary companies can become overvalued. The question isn't whether Nvidia will be crucial to computing's future (it almost certainly will be), but whether today's share price has already baked in several years of perfection.

When insiders sell during such frenzied periods... well, they might just be telling us something about price, if not prospects.

The Bigger They Are, The Easier They Sell

There's another angle here that doesn't get enough attention: what I've come to think of as the "liquidity ladder."

As companies grow massive (and Nvidia's market cap is, frankly, mind-boggling), insiders gain the ability to dump significant portions of their holdings without tanking the stock. The sheer trading volume and market cap provide cover for these sales.

In smaller companies? Try selling a billion dollars' worth of stock and see what happens to the share price. It wouldn't be pretty.

This creates an interesting paradox—the bigger and more successful a company becomes, the easier it is for insiders to reduce their stakes without sending negative signals. Though, judging by some recent market reactions, maybe those signals are getting through anyway.

We've Seen This Movie Before

This isn't the first time we've watched tech executives cash in big during boom times. I remember covering Amazon in the early 2010s when insiders regularly liquidated shares during various peaks. Apple executives have been selling for decades. Microsoft's leadership team has steadily reduced positions over time.

And yet... these companies delivered spectacular returns for patient investors.

The pattern typically unfolds something like this: insiders sell during peak optimism → retail investors charge in, thinking they're getting validation → reality eventually falls short of stratospheric expectations → a correction occurs → long-term investors who stick around ultimately do fine.

(That middle part can be painful, though. Just ask anyone who bought Cisco at its 2000 peak how long they waited to break even.)

Smart Money vs. Retail Enthusiasm

What makes the current Nvidia situation particularly fascinating is the growing gap between professional investors and retail sentiment. While individual investors remain wildly bullish—just check any investment subreddit—some institutional managers have been quietly reducing exposure.

"It's not that we don't believe in the AI story," one portfolio manager at a large growth fund told me on condition of anonymity. "It's that we've seen what happens when too much optimism gets concentrated in too few names."

This creates a fascinating market dynamic—almost a game theory problem—where different participants with different time horizons and risk tolerances make opposing moves that are entirely rational within their own frameworks.

So What's An Investor To Do?

If you're a long-term Nvidia believer who understands the business fundamentals, this insider selling probably shouldn't change your thesis. The AI revolution is real. The company's technological leadership is formidable. The growth story remains intact.

But... if you're trading on momentum or FOMO, or haven't really thought about what Nvidia is actually worth independent of what others are willing to pay for it today? Maybe take a breath.

When the people who know the company best are reducing their exposure, it's at least worth asking why—even if the answer might be as simple as "diversification" or "I finally want to enjoy some of this wealth I've created."

I've been tracking semiconductor cycles since the early 2010s, and one consistent lesson stands out: the business performance and stock performance don't always move in lockstep. Nvidia's business could continue executing flawlessly while its stock takes a significant breather.

In fact, that's exactly what happened in 2018 and again in 2022. And it'll probably happen again.

Perhaps the most rational approach is the one seemingly being taken by Nvidia's own leadership: maintain substantial skin in the game while acknowledging that concentration risk is real and diversification has merits.

After all, even the brightest minds in semiconductors understand you shouldn't put all your chips in one place—no matter how brilliant those chips might be.

stenciled clearly on its hull

• A handful of anxious-looking passenge")

scene of a small electronics repair workshop in Shenzhen. In the foreground, a focused technician in a simple work apron uses precision tools and a magnifying lamp to repair a disassembled Nvidia H100 GPU")

set on a sleek wooden desk in a bright, modern office. On the left end of the beam sits a neat stack of US dollar bills, on the right end a confident investo")