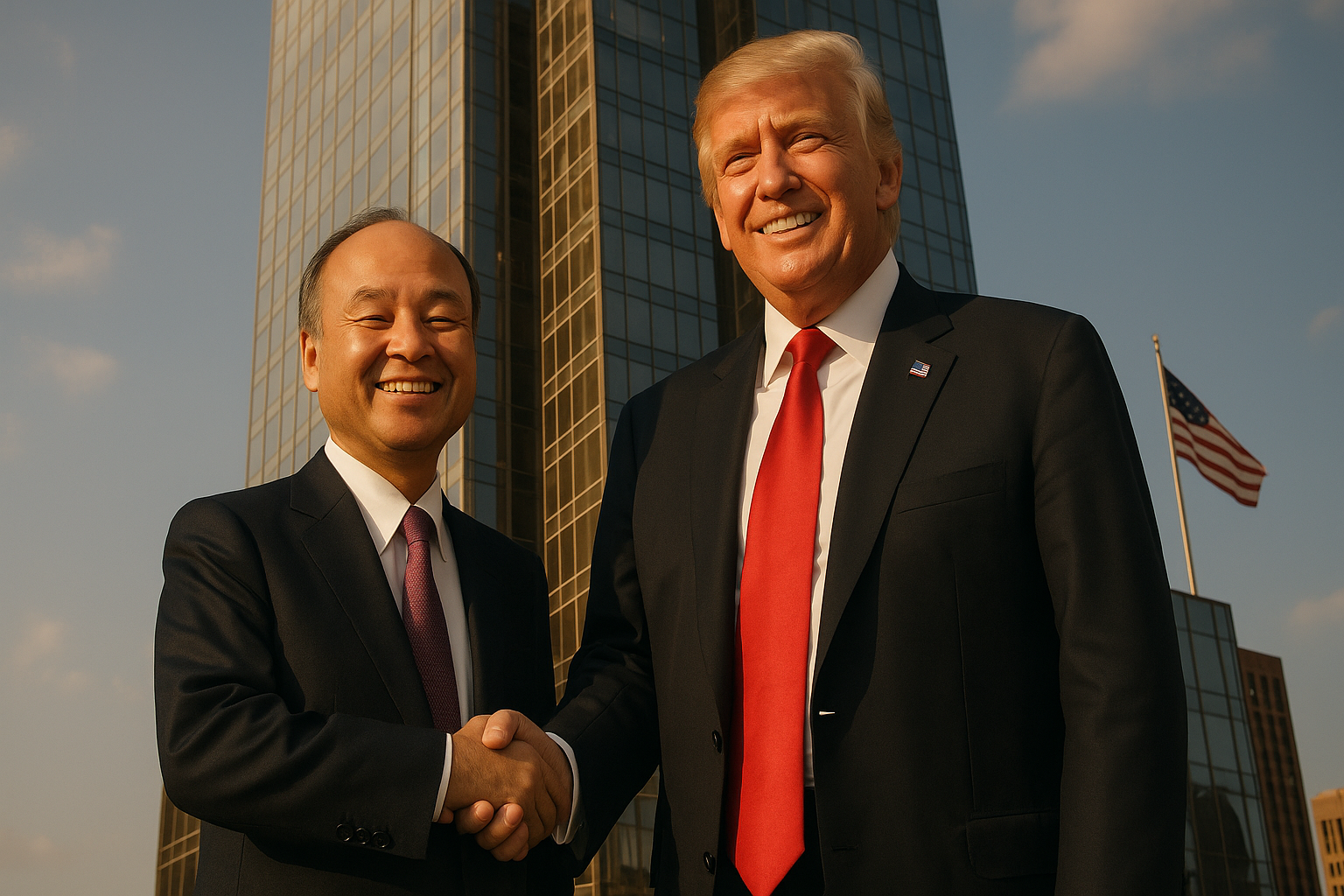

The moment was pure theater. Trump Tower, December 2016. A beaming president-elect stood shoulder-to-shoulder with a Japanese billionaire who'd just pledged a staggering $50 billion investment in American business. Donald Trump, never one to undersell a victory, immediately fired off a tweet: "Masa said he would never do this had we not won the election!"

And just like that, Masayoshi Son, founder of SoftBank and one of Asia's richest men, wrote himself into the Trump narrative.

I've been covering the intersection of business and politics for years, and let me tell you—this wasn't just another corporate photo op. It was the opening gambit in what would become one of the more fascinating corporate-political relationships of the Trump era. A relationship that, frankly, shouldn't have worked at all.

Think about it. The America First president and a Japanese tech investor with Saudi backing and Chinese business interests? Not exactly a natural match. And yet...

Son—or "Masa" as Trump preferred—had figured out something crucial that many corporate leaders missed. The currency of flattery in Trump's economy trades at premium rates. Always has.

"What Son did was borderline brilliant," a former Commerce Department official told me over coffee last month. "He repackaged existing investment plans into a gift-wrapped political offering."

Let's be clear about something: that $50 billion? It wasn't exactly fresh capital. Much of it represented previously planned investments through SoftBank's Vision Fund. But the presentation? Chef's kiss.

The Masa method for managing Trump followed a pattern we've seen before, but with a distinctively international twist:

First, establish personal rapport. Second, position yourself as a job creator (Trump's favorite kind of person). Third, align rhetorically with administration priorities. Finally, extract whatever regulatory goodwill you can.

And extract he did. When Sprint—controlled by SoftBank—sought merger approval with T-Mobile, things that initially looked dicey somehow... worked out. The deal went through in 2020 after initially facing serious regulatory headwinds.

Coincidence? Maybe. But Washington runs on relationships, and Son had cultivated one with the relationship-broker-in-chief.

What's particularly striking about this whole arrangement is how it contradicted the administration's broader stance toward foreign investment. Chinese companies faced unprecedented scrutiny, yet SoftBank—despite significant business interests in China—navigated the administration with remarkable dexterity.

There's something almost poetic about the Trump-Son connection. Both men are known for their outsized bets and theatrical business personas. Trump with his golden escalators; Son with his $100 billion Vision Fund and investments in everything from office sharing (the WeWork disaster) to dog-walking apps (remember Wag?).

Both have experienced spectacular successes... and equally spectacular flameouts. The WeWork implosion alone cost SoftBank billions—not unlike some of Trump's Atlantic City casino adventures in terms of sheer financial carnage.

Look, SoftBank's investment strategy under Son sometimes resembled Trump's own business approach: big, splashy moves designed partly for their announcement value. The Vision Fund's approach often seemed to be "growth at all costs"—dump gasoline on startups until they become too big to fail. It's putting your name in giant gold letters across the Manhattan skyline, but with venture capital.

How did Son pull this off? How did a Japanese company, backed by Saudi money, investing heavily in Chinese technology, somehow position itself as a champion of American jobs during the peak of America First economics?

The inconsistency is striking. In theory, America First meant viewing foreign investment with suspicion. In practice? It meant embracing foreign capital when it arrived with sufficient flattery and job promises—regardless of whether those promises fully materialized (and they often didn't).

I spoke with three former administration officials who confirmed that Son maintained access few foreign business leaders enjoyed. One called him "the exception that proved the rule" in Trump's approach to international business.

There's a lesson here that extends beyond the Trump years. As we move deeper into an era where geopolitics and business strategy are increasingly inseparable, the Son playbook deserves careful study.

For corporate leaders navigating today's fractured geopolitical landscape, there's something both instructive and slightly unsettling about how effectively Son played the game. It worked because he understood that beyond the policy positions and ideological statements, business diplomacy often operates at the level of personal psychology.

Sometimes the most effective strategy isn't about the most sophisticated regulatory approach—it's about figuring out what makes the person across the table feel like a winner.

And Masa Son? He made Trump feel like exactly that. The rest was just... details.