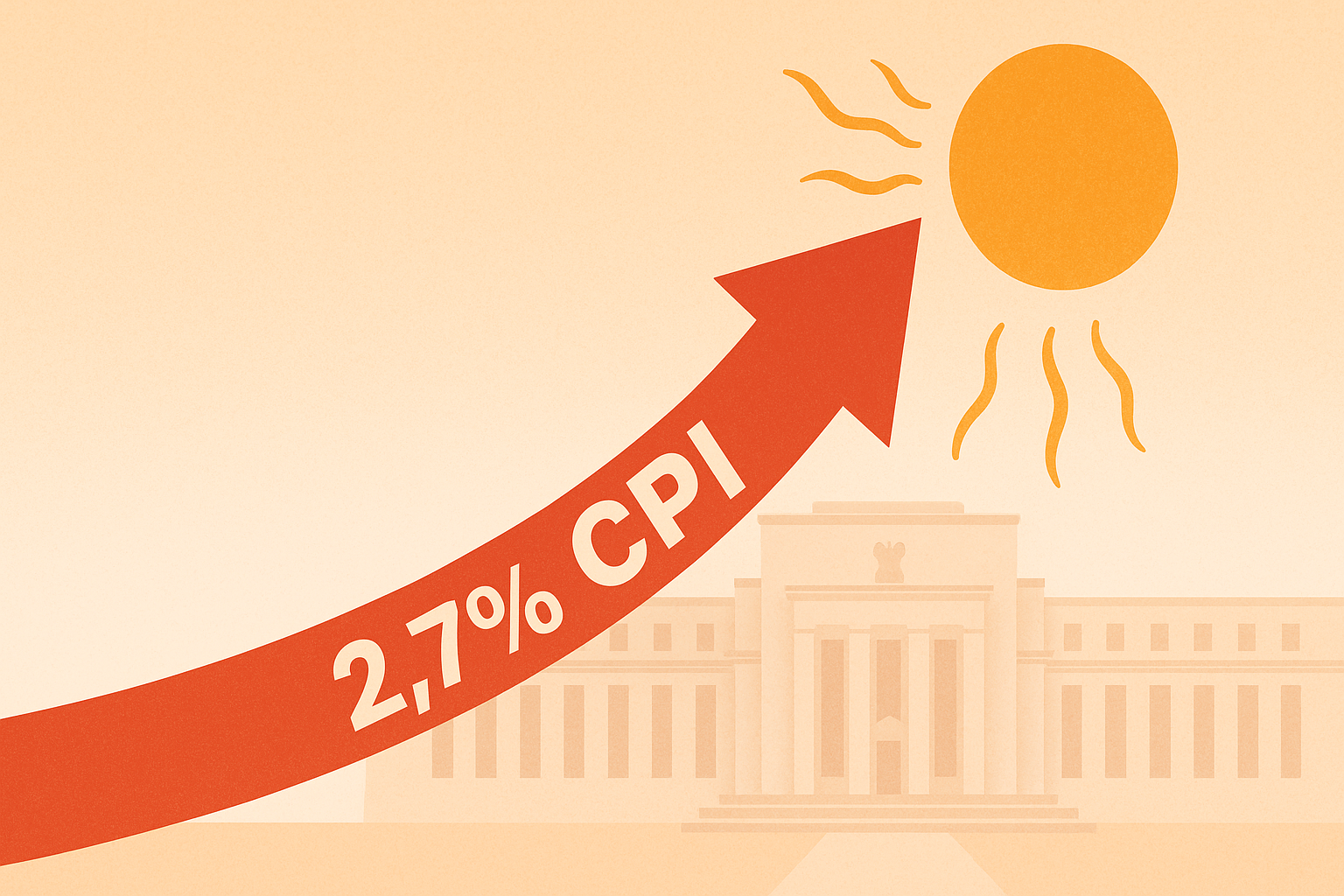

Inflation is making a comeback—and it's not the reunion tour anybody asked for. Fresh Consumer Price Index data shows prices climbing at a 2.7% annual clip in June, stubbornly refusing to cool despite the Fed's year-long interest rate assault.

Let me put this in perspective. I've been tracking these inflation numbers since before the pandemic (yes, my idea of weekend fun sometimes involves spreadsheets of PCE data), and there's something particularly annoying about this recent uptick. After watching inflation gradually step down over months, giving policymakers room to breathe, we're suddenly seeing a reversal that throws the Fed's neat narrative into disarray.

The breakdown tells a complicated story. While goods inflation has largely calmed down—remember those supply chain nightmares?—services inflation remains hot. And housing costs? They're still running wild, making up about a third of the CPI calculation and showing little sign of surrender.

I've found it useful to think about inflation as having three distinct sources: supply problems (think pandemic disruptions, war in Ukraine), demand pressures (all those stimulus checks and revenge vacations), and expectations (businesses and workers building future price increases into their plans). The Fed can influence demand but has little control over supply chains, while expectations... well, that's the tricky middle ground.

What's giving Powell headaches is that all three are still in play, though the mix has shifted dramatically from a year ago.

This 2.7% reading leaves the Fed in what my old economics professor would call a classic "trembling hand" dilemma. They've signaled they want to cut rates to avoid crushing the economy, but each inflation surprise makes their finger hesitate over the button. Markets that confidently predicted multiple 2024 rate cuts are now scrambling to recalibrate faster than a barista during morning rush.

Picture yourself as an FOMC member right now. You've kept rates at painful highs for nearly a year. The job market is softening but hasn't collapsed. Growth remains decent. Yet inflation refuses to hit that 2% target you've promised. It's monetary policy purgatory—nothing quite bad enough to force action, nothing good enough to celebrate.

This reminds me of watching Greenspan navigate the 1998 Russian debt crisis, though with a twist. Back then, he cut rates despite solid economic data because financial markets were in turmoil. Today's Fed faces the opposite challenge—they want to cut despite inflation being in turmoil because they fear where the labor market might be heading. But while Greenspan could claim market stability as part of the Fed's mandate, Powell can't easily explain away another inflation miss.

The market reaction? Predictably unpredictable. Stocks stumbled on the news, then rallied, then wobbled again—like someone who's had three too many drinks insisting they're "totally fine." The dollar strengthened, gold retreated a bit, and bitcoin did its bitcoin thing (which is to say, it moved dramatically for reasons nobody can fully explain).

For regular folks—you know, the people actually living with inflation rather than just analyzing it—this resurgence feels like stepping on a Lego in the dark. Real wages had finally started outpacing inflation, giving workers some breathing room. Now that progress looks shaky. The average household is still spending roughly $700 more monthly than before the pandemic for the same basket of goods. That's not an abstract statistic; it's parents debating whether to cut back on summer activities or continue draining their savings.

Is this a blip or the start of another stubborn plateau? Hard to say. Economic data rarely delivers the clean, straight-line narratives we crave. Remember "transitory inflation"? Or when the Fed's projections showed no rate hikes for years right before they launched the most aggressive tightening cycle in decades?

Look, the journey from 3% to 2% inflation was always going to be the toughest part. We've already picked the low-hanging fruit—fixed supply chains, normalized energy prices. What remains are the stickier elements: shelter costs that move with frustrating lags, service prices tied to wage growth, and the background hum of inflation expectations that have settled above target.

For now, Powell and company will likely hold steady, watching the data and reminding us at every opportunity that policy remains "data dependent"—central banker speak for "we're watching this situation as closely as you are, but with fancier charts."

The September rate cut that seemed like a lock just weeks ago now looks more like a coin flip with a slight bias—heads they cut, tails they wait. And markets, which hate uncertainty more than bad news, will continue their nervous dance until clarity emerges.

I've covered enough Fed cycles to know one thing for certain: inflation, like most economic forces, rarely gives us satisfying conclusions. It's messy, lagged, and influenced by countless factors beyond any single institution's control. The Fed is essentially steering an oil tanker through fog with controls that respond on a 12-18 month delay.

In the end, perhaps the most valuable approach for investors, policymakers, and regular folks alike is a healthy dose of humility about what we know and what we can control. In the meantime, that stubborn 2.7% figure reminds us that economics is more art than science—and sometimes, the canvas refuses to cooperate with the artist's vision.

scene of a typical suburban mailbox standing by a quiet street. The mailbox door is open and empty, its red flag raised. An envelope stamped “$2000 Stimulus Check” drifts away o")