The Federal Reserve's latest meeting minutes read like a high-stakes economic Choose Your Own Adventure novel, with policymakers mapping out very different potential paths for the U.S. economy—and disagreeing about which one we're currently on.

Fed officials find themselves increasingly divided over the economy's trajectory, though they broadly agreed interest rates should remain restrictive "for some time." Translation: Don't expect rate cuts tomorrow, folks.

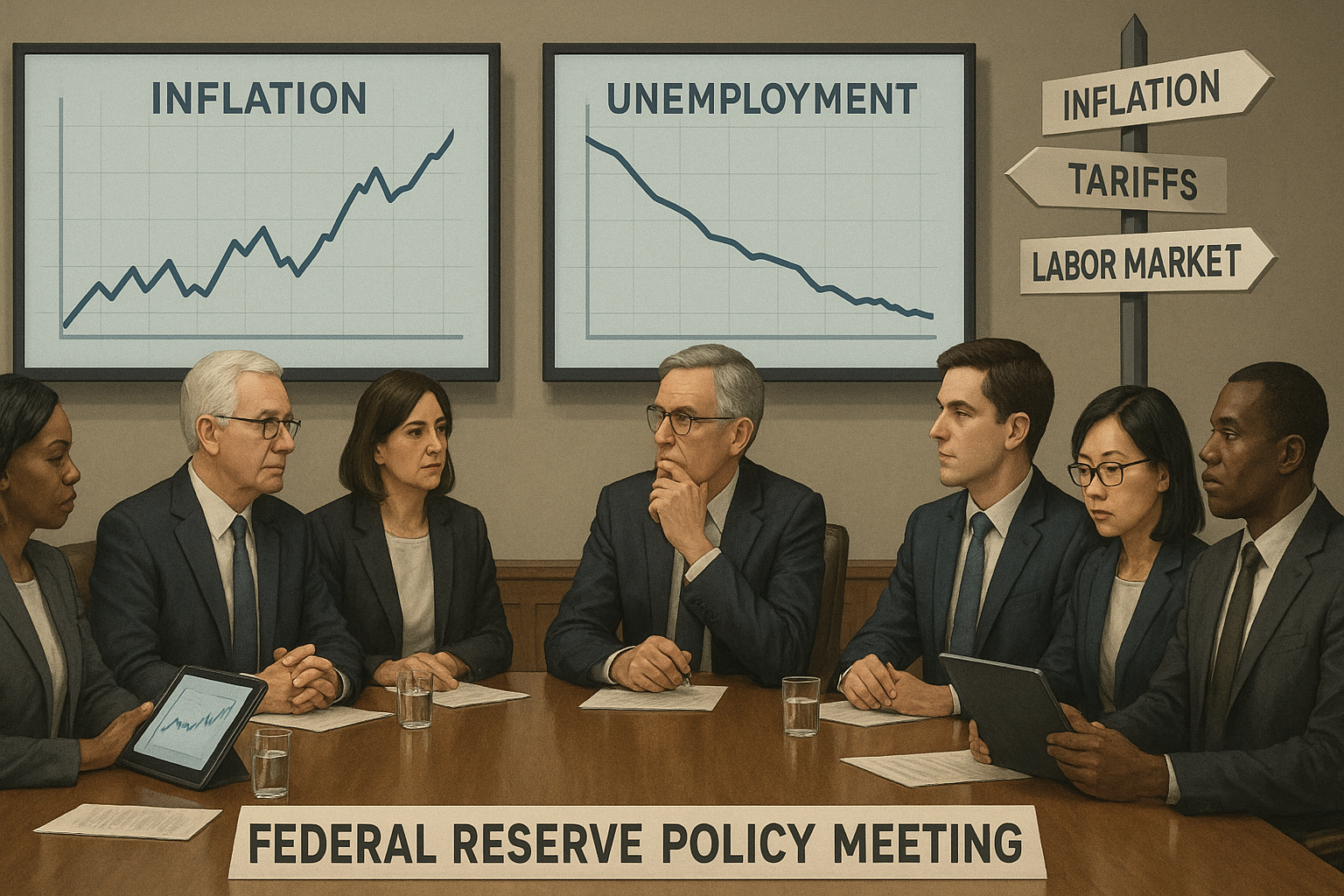

The minutes reveal a committee grappling with three major economic bogeymen simultaneously: stubborn inflation that won't quite die, potential new tariffs that could reignite price pressures, and a labor market that's showing... well, something. Exactly what that something is depends entirely on which Fed official you ask.

I've been covering Fed meetings since the pre-pandemic era, and I can't remember a time when the range of concerns was quite this diverse. It's like watching a group of meteorologists argue about whether those clouds on the horizon mean clear skies, scattered showers, or a hurricane.

The tariff question particularly stands out. Several officials explicitly worried that new or higher tariffs—the kind both presidential candidates have floated—could pump unwanted oxygen into inflation's embers just as they've started cooling. We've seen this movie before. The 2018-2019 tariff rounds definitely nudged prices upward in affected sectors.

"Participants noted that an escalation of trade restrictions could put upward pressure on prices," the minutes stated, in classic Fed understatement.

Look, anyone who's studied tariffs knows they function essentially as a consumption tax paid primarily by domestic consumers and businesses, not foreign exporters. The costs ripple through supply chains like a stone thrown in a pond.

Meanwhile, the labor market has become something of an economic Rorschach test. The minutes noted "signs of cooling," but officials differed sharply on whether that represented healthy normalization or the beginning of something more troubling.

The unemployment rate now sits at 4.1%—historically still quite low. But as one Fed official pointed out during the meeting (the minutes don't name names), it's the pace of change that sometimes signals trouble. The three-tenths increase we've seen recently has, in past cycles, occasionally preceded more significant deterioration.

(Interestingly, just days after this meeting, the April jobs report came in hotter than expected, throwing yet another curveball into the Fed's deliberations.)

What makes the Fed's position particularly tricky is that they're navigating this uncertainty while inflation—though improved—remains stubbornly above their 2% target. It's the central banking equivalent of trying to land a plane in fog while the instruments show conflicting readings.

"Several participants noted that recent inflation readings had not strengthened their confidence that inflation was moving sustainably toward 2 percent," the minutes said.

The financial markets, meanwhile, continue behaving like impatient children on a road trip, constantly asking "are we there yet?" regarding rate cuts. Futures markets are pricing in multiple reductions this year, more aggressive than what the Fed's own projections suggest.

This disconnect isn't new. I've watched it play out for months now. Markets essentially believe economic weakness will force the Fed's hand, while policymakers maintain they'll cut when—and only when—they have clear evidence inflation is truly contained.

So where does all this leave us? Pretty much exactly where we started—in a holding pattern of uncertainty.

The minutes suggest a committee genuinely divided on which risk deserves more weight: persistent inflation or economic deterioration. Chair Powell and his colleagues will continue analyzing each new data point, debating the risks, and reminding us they remain "data dependent"—a phrase that manages to be both entirely reasonable and completely unhelpful for anyone trying to predict their next move.

Until then... well, we watch and wait. The thrilling world of monetary policy continues.

scene showing a diverse group of job seekers—men and women of different ages and backgrounds—standing in a long queue outside a modern office building. In the window is a modest “Now Hiring” sign wi")

realistic digital illustration depicting a corporate “reality check”:

- A modern glass-walled boardroom with a long conference table

- On the far wall, a large screen displaying:

• The Salesforce logo in one corner")